Image credit: Pablo Merchan Montes, Unsplash

Image credit: Pablo Merchan Montes, Unsplash

As risks to our art collections evolve, so must our fine art insurance. Learn how to update your insurance strategy to protect your museum's collection.

Fine art insurance is a crucial tool for museums, ensuring that valuable works are protected against unforeseen risks. A recent webinar hosted by Artwork Archive featuring Adrienne Reid from Huntington T. Block provided best practices for risk management. In this article we break down the takeaways from the presentation.

Watch the recording of "Art Collection Insurance: What You Need to Know to Stay Protected."

Why insuring your art collection properly matters

Regardless of the size of your collection, art is vulnerable to risks such as theft, fire, natural disasters, and accidental damage. Fine art insurance is specifically designed to address the unique risks and needs associated with artwork and cultural property, which general insurance policies often do not cover adequately.

For instance, did you know that your packing crates, installation material and technical equipment are covered in fine art insurance?

Understanding what your insurance may not cover

It's also important to know what your insurance plan may not cover. Adrienne shared standard exclusions:

-

Wear and tear, gradual deterioration, inherent vice

-

Repairing, restoration or retouching

-

War risks

-

Government action (seizure & confiscation)

-

Nuclear risks

Assess your museum's risk exposure

Adrienne provided a comparison between the frequency and severity of museum claims in the past three years so that museums can understand the risks and perils their institutions may be exposed to.

Chart provided by Huntington T. Block

Chart provided by Huntington T. Block

What did we learn? Losses in transit and water damage are severe and some of the most frequent risks. Whereas, catastrophic losses from fires, floods, and theft don’t happen very often.

There are procedural risks that can be avoided with better handling of artwork like visitor damage and vandalism. And, then there’s the minor damages that occur during transit or from small restoration needs. Adrienne explained: “Those tend to be more frequent, but less severe. Usually those are things that can be repaired, but still are an important thing to keep in mind.”

Understanding these risks help institutions assess their risk exposure and tailor their policies accordingly.

Evolving risks and policy exclusions

With the increasing frequency of natural disasters such as hurricanes, wildfires, and floods, insurers are adapting policies to reflect these evolving risks. Adrienne highlighted the importance of wind protection coverage in storm-prone regions.

Adrienne also highlighted relatively new exclusions like terrorism, communicable disease and cyber attack. And she's witnessed some museums consider additional coverage for terroris,.

Mitigating human error in emergency preparedness

Even with a well-crafted and detailed emergency preparedness plan, human error remains a significant factor in risk management. Adrienne emphasized the necessity of onboarding staff and regularly practicing emergency procedures to ensure swift and effective responses during crises. Conducting drills, reviewing protocols, and engaging team members in preparedness efforts can greatly reduce the likelihood of costly mistakes during an emergency.

Key insurance clauses explained

Valuation clause

A valuation clause in a fine art insurance policy specifies how much the insurance company will pay out in the event of a claim. The valuation clause is based on a variety of factors, including the artwork's value at the time of the loss.

Artwork Archive Tip:

Seeking advice on how to get your artworks and collection appraised? Check out our Inventory Management and Appraisals recorded webinar with Winston Art Group.

Partial vs. Total Loss

The webinar also highlighted the importance of understanding how policies handle partial versus total loss scenarios. In cases of partial loss, insurers may cover restoration costs, while total loss involves compensation for the full insured value of the item.

Loss Buy Back and Salvage

Additionally, institutions should be aware of clauses like Loss Buy Back and Salvage. After an insurance company declares a piece of art as a “total loss” due to damage, the clause allows the owner to buy back the damaged artwork at a significantly reduced price, essentially acquiring it as “salvage art” which can then be repurposed, displayed as is, or used by artists to create new works.

Pairs & Sets Clause

One of the most popular takeaways for webinar attendees was the Pairs & Sets clause, which refers to works part of a series, like a triptych, or a set like a tea cup and saucer. If one piece in a set is damaged or lost, this clause ensures appropriate compensation for the diminished value of the remaining pieces.

Are your loans and exhibitions properly insured?

Many collectors and institutions frequently loan artworks for exhibitions or research purposes. Ensuring proper insurance coverage for loans is critical, as artworks in transit or displayed at external venues are exposed to additional risks.

Adrienne stressed the importance of a loan agreement to establish insurable interest, valuation and the insurance responsibility period. Having documentation and agreed upon values will avoid potential conflict.

When lending pieces, it is essential to:

-

Clarify insurance responsibilities: Determine whether the borrower or lender is responsible for insurance coverage and ensure all agreements are documented. For instance, who is responsible for the artwork while it is in transit?

-

Assess coverage limits: Verify that the policy covers potential damages or loss during transport, installation, and exhibition.

-

Adrienne provided a tip of looking at your upcoming year’s temporary exhibition calendar and updating your insurance to reflect, roughly, the approximated values of the artworks.

-

-

Understand loan agreements: Work with legal and insurance professionals to review contractual terms, including liability and indemnification clauses.

-

Monitor condition reports: Conduct pre- and post-loan condition assessments to track any changes or damage that may have occurred. Make sure you have photos!

Having a loan agreement ensures that both lenders and borrowers are protected, reducing financial and legal risks associated with temporary transfers of artwork.

Did you know that you can track inbound and outbound loans in Artwork Archive? Always have loan agreements, lender contact information and values on hand. Learn more about loan tracking here.

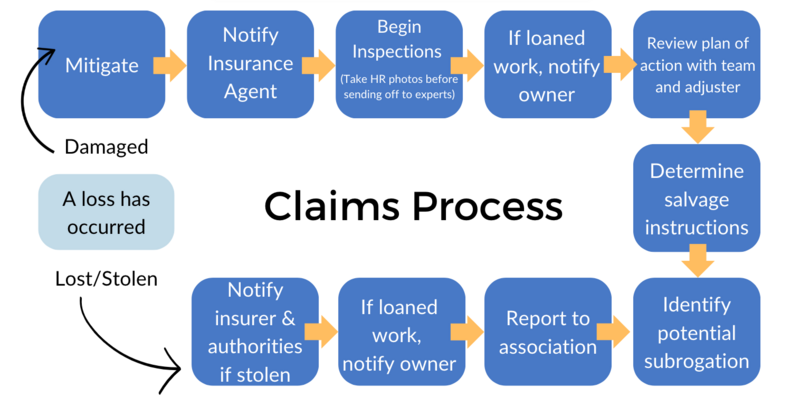

Navigating the claims process

If you have to file an insurance claim, are you prepared? Here is an overview of the process.

Common claim pitfalls

- No action leads to more significant damages

- Lack of a plan causes delays

- Lack of communication causes confusion and delays

- Lack of leadership causes chaos

- Lack of documentation causes delays and expense

Artwork Archive Tip:

Don't delay your claims process with a lack of documentation. Be prepared. Record and have access to the following documentation in a collection management system like Artwork Archive.

- Receipts & bills of sale

- Appraisals with artwork values

- Photographs

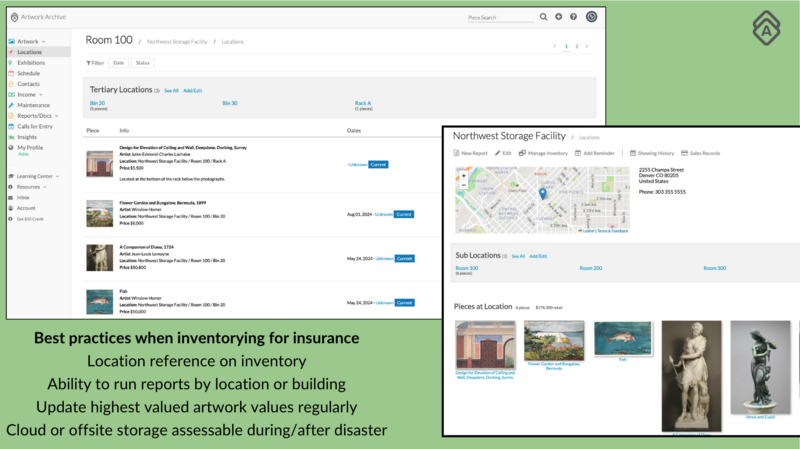

The importance of art databases for documentation

Proper documentation is essential not only for claims but also for maintaining an organized and secure record of your collection. With an art collection management system like Artwork Archive you’ll have a centralized location for all detailed records and documents (like provenance, appraisal values, images and condition reports)–all of which can be accessed by teammates handling insurance or loans whether that’s the registrar, development officer or curator.

Furthermore, a collection management system streamlines communication with insurers and appraisers, making it easier to provide the necessary documentation during claims or valuation updates. Investing in an art database not only protects your collection but also enhances its management and long-term care.

Slide from "Art Collection Insurance: What You Need to Know to Stay Protected" webinar

Slide from "Art Collection Insurance: What You Need to Know to Stay Protected" webinar

Just like a collection management system, fine art insurance is an essential aspect of responsible art ownership.

By securing tailored policies, conducting regular appraisals, implementing risk management strategies, and utilizing a collection management system, institutions can protect their valuable assets against unforeseen events.

Investing in the right insurance ensures the longevity and security of your collection for generations to come.